Finat on business climate in label printing industry

The European Label Forum provided critical analysis of the current economic conditions, challenges and opportunities facing the sector.

The 2024 Finat European Label Forum (ELF) in Athens, Greece, has kicked off with a session focused on the general business climate within the label printing industry, which set the stage for the forum by providing a critical analysis of the current economic conditions, challenges and opportunities facing the sector.

As label converters and industry stakeholders grapple with economic uncertainty, inflation, and changing consumer behavior, the insights from this session are invaluable for navigating the complex landscape ahead.

Challenging economic Landscape

According to Finat, the label printing industry is currently operating in a challenging economic environment marked by several key factors:

- Persistently high inflation: Inflation continues to be driven by rising energy costs, which in turn have led to higher expenses for both consumers and businesses. This inflationary pressure has necessitated interest rate hikes aimed at curbing inflation, but these measures have also increased the cost of borrowing, complicating investment decisions for many companies.

- Slow economic growth: Several European countries are facing what can be described as a ‘technical recession’, with economic growth remaining sluggish. While the labour market remains tight, contributing to wage increases, this dynamic also exacerbates inflationary pressures, further complicating the business environment for label converters.

- Political uncertainty: Elections and changes in government across Europe have added another layer of uncertainty, making it more difficult for businesses to plan and invest with confidence. This political volatility is contributing to the broader economic challenges faced by the label industry.

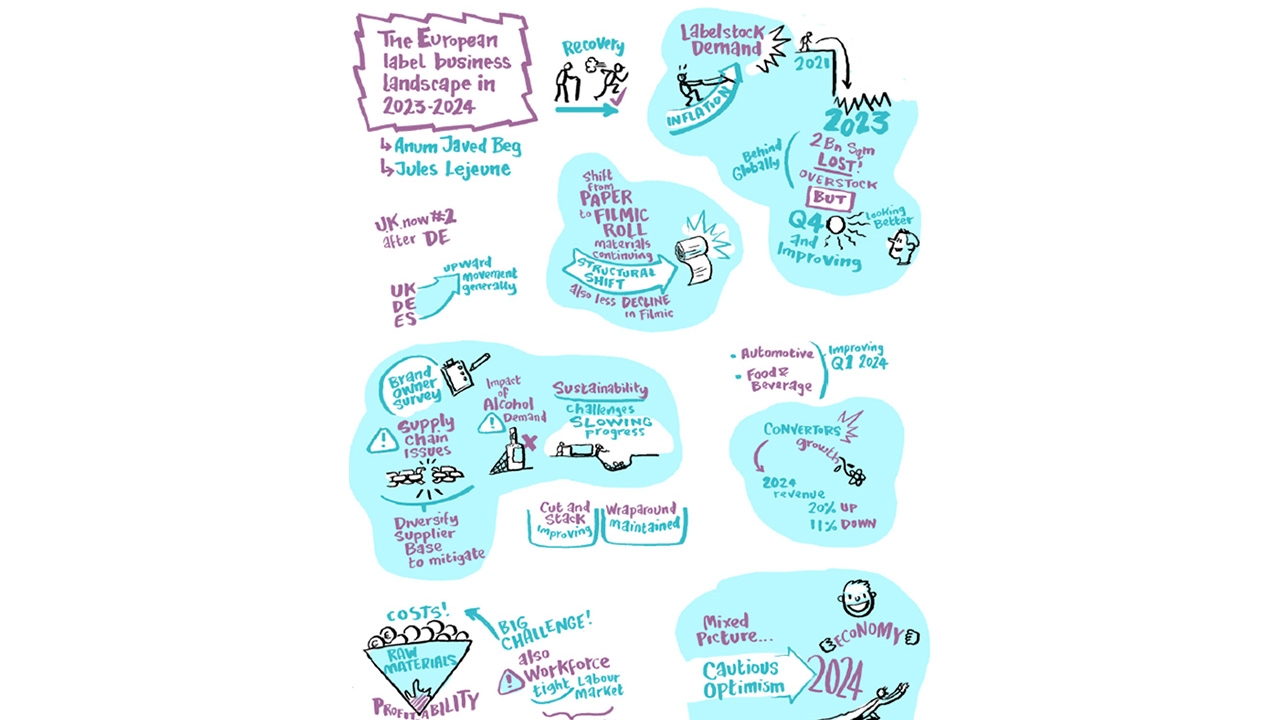

- Excess stock issues: The label industry has been dealing with the consequences of excess stockpiling, which occurred during the supply chain disruptions of 2022. This has resulted in a significant drop in demand for new labelstock in 2023, adding to the industry's current difficulties. In the first half of 2024 however, stock levels appear to have returned to normal.

Labelstock demand and market dynamics

According to data presented at the forum, the European label market experienced a notable downturn in 2023. Overall labelstock demand decreased by 25.8 percent, bringing it back to levels not seen since 2013. This decline was largely due to destocking efforts as converters worked through excess inventories built up during the supply chain disruptions of the previous year. In the first half of 2024, however, labelstock demand recovered strongly, with year-on-year increases of 29.4 and 22.7 percent respectively.

Regardless of the volatility experienced in previous years, the demand for different types of labelstock has also seen structural shifts:

- Filmic roll labelstocks: Despite the overall market contraction, the share of filmic roll labelstocks has continued to grow, reaching nearly 30 percent of the market in 2023. This growth is driven by the increasing use of polypropylene (PP) rolls, particularly in high-quality product decoration films for sectors like health, beauty, and food, where transparency and the "no-label look" are highly valued.

- Direct thermal labels: There has been a rise in the use of direct thermal labels, particularly in applications requiring short-term variable data, such as online shopping logistics and inventory management. This trend reflects the broader shift towards e-commerce and process automation.

- Decline in white uncoated and sheet labels: In contrast, the market share for white uncoated rolls and sheet labels has halved since 2005, reflecting changing consumer preferences and the increasing importance of brand differentiation through high-quality packaging.

Market outlook and future drivers

Looking ahead, the forum highlighted cautious optimism tempered by significant risks and uncertainties:

- Economic recovery: There is an expectation of moderate economic recovery as inflation gradually eases and consumer confidence improves. This recovery, however, is likely to be uneven, with some regions and sectors rebounding faster than others.

- Sustainability and regulatory pressures: Sustainability remains a key concern for consumers and, by extension, brand owners. Recent revisions to Extended Producer Responsibility (EPR) schemes are pushing companies to take greater responsibility for the environmental impact of their products, including labels. This is driving demand for eco-friendly materials, such as recycled paper and biodegradable substrates, and pushing companies to optimise their label procurement processes to reduce costs and waste.

- Technological innovation: Investment in digitalisation, automation, and smart labelling technologies is expected to increase as companies seek to enhance efficiency and stay competitive. These innovations are likely to play a critical role in shaping the future of the label industry, particularly in areas like process automation and supply chain transparency.

- Geopolitical and economic risks: Ongoing geopolitical tensions and other international uncertainties continue to weigh on economic sentiment. Structural reforms are needed to boost productivity and support long-term growth, but these are likely to be slow to materialise, adding to the uncertainty faced by businesses.

The general business climate session at the European Label Forum 2024 underscored the complexities and challenges facing the label printing industry. While there are significant headwinds, including economic uncertainty, inflation, and regulatory pressures, there are also opportunities for growth and innovation. By staying informed and agile, industry stakeholders can navigate these challenges and capitalize on the emerging trends that will define the future of the label printing industry.

Stay up to date

Subscribe to the free Label News newsletter and receive the latest content every week. We'll never share your email address.